Since the treasury stock is owned by the S-corp, it does not violate the one class rule. Therefore, so long as the state permits a corporation to hold treasury stock, an S-corp can as well.

Does treasury stock reduce S Corp basis?

S corporations are not taxed for owning treasury stock because there are no voting rights or distribution rights, according to Legal Beagle. A buyout reduces the current assets of an S corporation’s balance sheet, which has a negative effect on the company’s cash balance.

Does treasury stock affect shareholder basis?

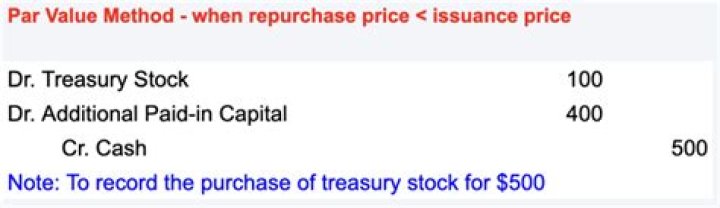

Understanding Treasury Stock (Treasury Shares) Treasury stock is a contra equity account recorded in the shareholder’s equity section of the balance sheet. Because treasury stock represents the number of shares repurchased from the open market, it reduces shareholder’s equity by the amount paid for the stock.

Does treasury stock reduce stock basis?

Because treasury stock represents the number of shares repurchased from the open market, it reduces shareholder’s equity by the amount paid for the stock.

What increases an S corp shareholders stock basis?

Stock basis is adjusted annually, as of the last day of the S corporation year, in the following order: Increased for income items and excess depletion; Decreased for distributions; Decreased for non-deductible, non-capital expenses and depletion; and.

Why would a company buy treasury stock?

Treasury stock is often a form of reserved stock set aside to raise funds or pay for future investments. Companies may use treasury stock to pay for an investment or acquisition of competing businesses. These shares can also be reissued to existing shareholders to reduce dilution from incentive compensation plans.

How many shares of stock does S corporation have?

Shareholder Z owns two shares of stock in an S corporation. Only 10 shares of stock are issued and outstanding as of December 31, 2000. The basis in the two shares is $20.

How to record a buyout of an S-Corp shareholder?

You have Treasury Stock for the purchase price (assuming your state allows Treasury stock) and a Note Payable for the amount owed. You will also need to show the ownership change (ProSeries Professional has worksheets for this but I do not know about PTO).

Can A S corporation stock distribution be tax free?

A distribution to a selling shareholder of an S corporation will be tax-free to the shareholder to the extent that the amount of the distribution does not exceed either the shareholder’s tax basis or the amount of the company’s AAA.

What happens when a shareholder leaves a C corporation?

A shareholder departing from either a C corporation or an S corporation may sell his or her shares of stock to some or all of the other shareholders. He or she will realize gain equal to the amount paid for the shares over his or her adjusted basis in the shares.