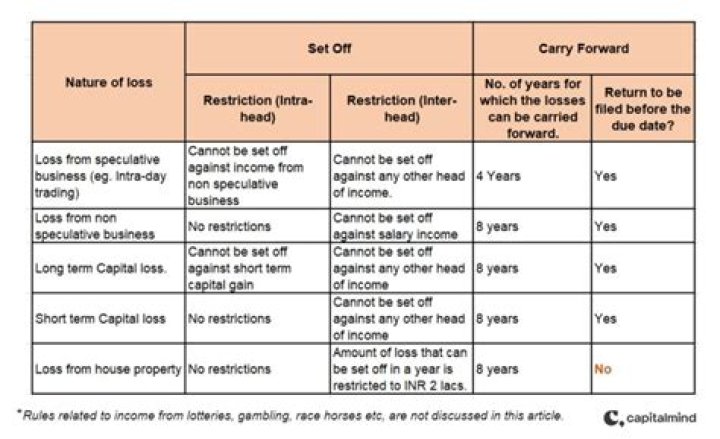

A tax loss carryforward allows taxpayers to use a taxable loss in the current period and apply it to a future tax period. Capital losses that exceed capital gains in a year may be used to offset ordinary taxable income up to $3,000 in any future tax year, indefinitely, until exhausted.

A Tax Loss Carry Forward carries a tax loss from a business over to a future year of profit. For losses arising in taxable years beginning after Dec. In years before 2018, tax loss carryforwards could only be used for 20 years, but under the new tax law, tax losses may be carried forward indefinitely.

How many years can I take a loss on my business?

The IRS will only allow you to claim losses on your business for three out of five tax years. If you don’t show that your business is starting to make a profit, then the IRS can prohibit you from claiming your business losses on your taxes.

Do you have to be in business to have a Nol?

By the way, you don’t have to be in business to have an NOL. There are several items that can cause an NOL, such as casualty and theft losses, but business losses are the most common cause. Who Can Claim a Net Operating Loss?

Is the net operating loss included in the NOL?

Certain types of losses and deductions are generally excluded from the NOL calculation, including: Most net operating losses are related to business losses. To take the loss, you must include it on your personal tax return.

Can a business carry a net operating loss back?

Deducting a Net Operating Loss. In the past, business owners could “carry a loss back”—that is, they could apply an NOL to past tax years by filing an application for refund or amended return. This enabled them to get a refund for all or part of the taxes they paid in past years. NOLs could generally be carried back two years.

Can a Nol be carried forward to a future year?

Any unused NOL amounts may be carried forward and deducted in any number of future years (under prior law, NOLs could be carried forward no more than 20 years). The TCJA also limits deductions of “excess business losses” by individual business owners.