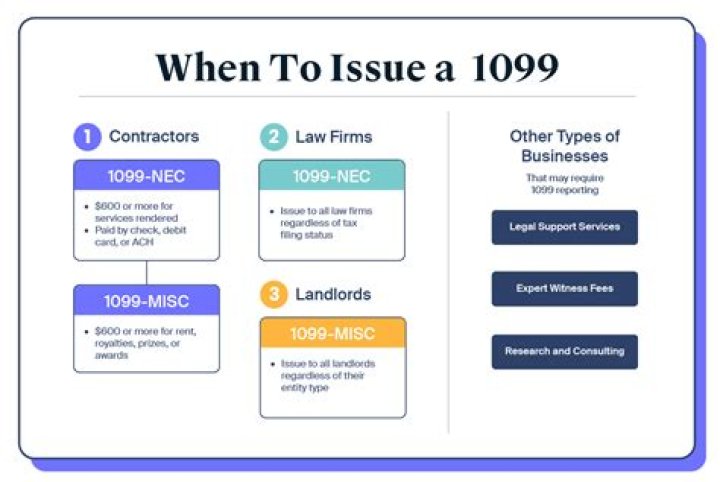

In general, payments to corporations do not need to be reported on a 1099-MISC; LLCs and partnerships are issued 1099s, unless they are taxed as S- or C-Corporations (you can determine this status from their W-9).

What changed on 1099?

New Form 1099-NEC The IRS has made big changes to the 1099-MISC form by reviving the 1099-NEC form. Beginning with the 2020 tax year (to be filed by February 1, 2021) the new 1099-NEC form will be used for reporting nonemployee compensation (NEC) payments. Boxes 5-7 are used to report any state withholding.

Sole proprietors, partnerships and limited partnerships all get 1099s if they hit the $600 threshold. The IRS lists other payment categories that don’t require a 1099, even if the recipient is not a corporation. Rent payments to property managers or real-estate agents rather than directly to the landlord.

Can You issue a 1099 to your husband?

If in fact you actually paid your husband then yes, you can issue a 1099 to him. You would deduct this as a business expense on Schedule C. You would need to provide a copies of the 1099-MISC to the IRS and your state tax office, and also file form 1096.

Where does the 1099 go in a partnership?

The 1099 is a 1099-MISC and proceeds in box 7. Taxpayer said 2016 was the first year that partnership disbursed funds and they issued a 1099-Misc. Peggy Sioux

Can a p’ship issue a 1099 MISC to a partner?

A p’ship should not issue a 1099-MISC to a partner for services. Instead, such payments should be treated as “guaranteed payments” and reported on the appropriate line of that partner’s K-1.

Do you have to issue a 1099-MISC for a lawsuit settlement?

You pay an individual at least $600 over the course of a year, provided this payment or payments was for a prize, rent, or service (including materials or parts). A lawsuit settlement that you have paid out also requires you to issue a 1099-MISC. This form is not required for personal payments, only for business payments.