When you and your spouse file your taxes together, taking the mortgage interest deduction is a simple matter of copying a number from your mortgage statement to Schedule A of your tax return. If you choose to file separately, you must claim your share of the mortgage interest on your individual Schedule A forms.

How do you claim mortgage interest on taxes?

You claim the mortgage interest deduction on Schedule A of Form 1040, which means you’ll need to itemize instead of take the standard deduction when you do your taxes.

Is mortgage interest separate from standard deduction?

The Tax Cuts and Jobs Act lowered the maximum mortgage interest deduction amount, but increased the standard deduction amounts….Mortgage interest deduction vs. standard deduction.

| Filing Status | 2019 Standard Deduction | Mortgage Balance needed to itemize |

|---|---|---|

| Head of Household | $18,350 | $520,000 |

When claiming married filing separately, mortgage interest would be claimed by the person who made the payment. Therefore, if one of you paid alone from your own account, that person can claim all of the mortgage interest and property taxes.

Taking the standard deduction means you can’t deduct home mortgage interest or take the many other popular tax deductions — medical expenses or charitable donations, for example.

How to deduct mortgage interest when filing separately?

How are mortgage interest and real estate taxes divided?

If each taxpayer paid one-half of the mortgage and real estate tax expenses, then each Schedule A should reflect one-half as deductions. Both of you should attach a statement to your Schedules A explaining how you’re dividing the mortgage interest and payments of real estate taxes.

Are there any changes to the mortgage interest deduction?

Owning your own home comes with some nice tax perks. One of them is the home mortgage interest deduction. The Tax Cuts and Jobs Act (TCJA) affected this deduction somewhat when it went into effect in 2018, but the legislation did not eliminate the deduction from the tax code entirely. 1 It just sets some limits and restrictions.

What was the mortgage interest deduction before the tax cuts and Jobs Act?

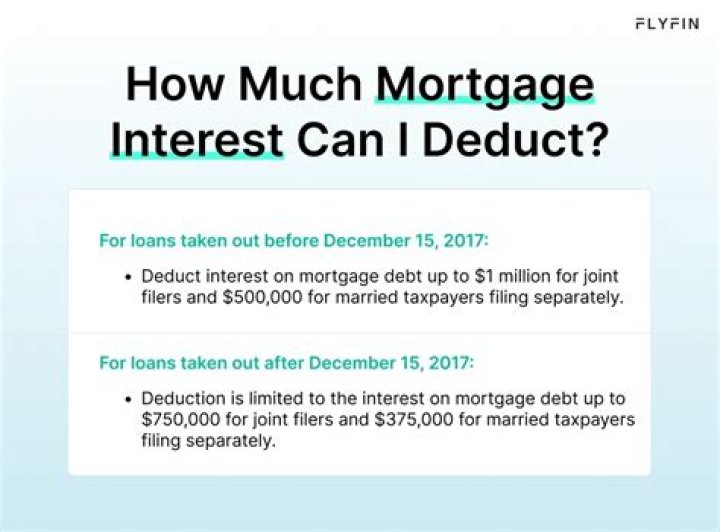

Before the Tax Cuts and Jobs Act, the mortgage interest deduction limit was $1 million. Today, the limit is $750,000. That means this tax year, single filers and married couples filing jointly can deduct the interest on up to $750,000 for a mortgage, while married taxpayers filing separately can deduct up to $375,000 each.