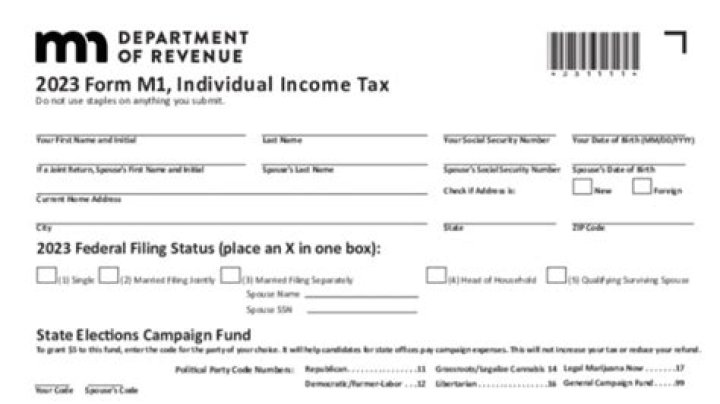

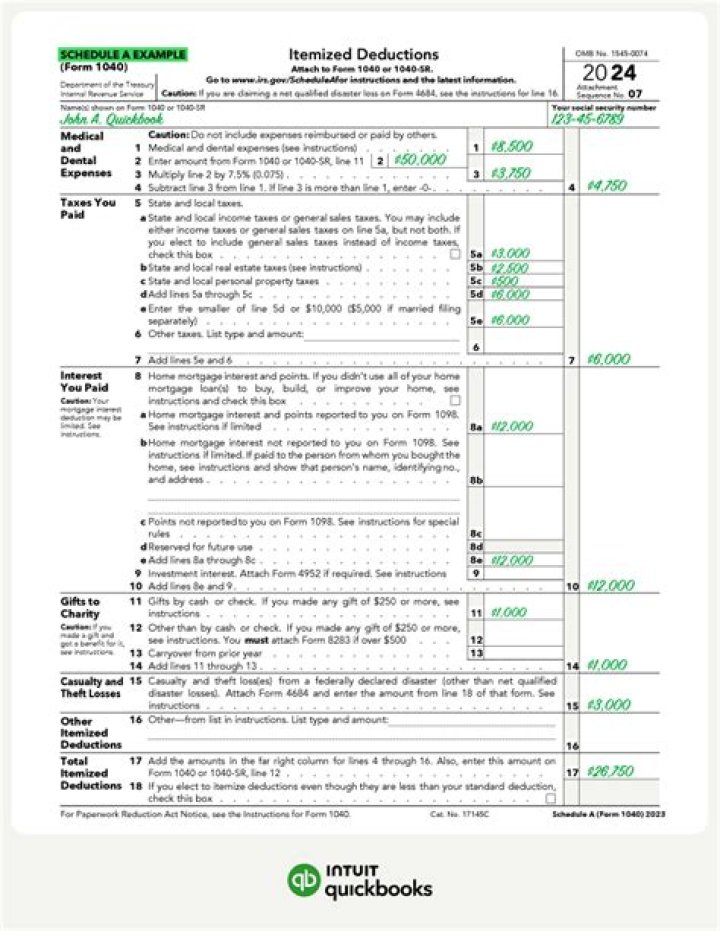

Casualty and theft losses are miscellaneous itemized deductions that are reported on IRS Form 4684, which carries over to the Schedule A, then to the 1040 form. Therefore, in order for any casualty or theft loss to be deductible, the taxpayer must be able to itemize deductions.

Claiming the Loss Individuals may claim their casualty and theft losses as an itemized deduction on Schedule A (Form 1040), Itemized Deductions (or Schedule A (Form 1040NR) PDF, if you’re a nonresident alien). Report casualty and theft losses on Form 4684, Casualties and Thefts PDF.

Can you claim being scammed on your taxes?

A personal casualty loss (including a theft) is deductible if you itemize deductions. If deductible, the loss must first be reduced by $100 (in 2009 – $500), and any remainder is deductible to the extent it exceeds 10% of your adjusted gross income. …

Do you have to itemize Casualty and theft losses?

Therefore, in order for any casualty or theft loss to be deductible, the taxpayer must be able to itemize deductions. If this is not possible, then no loss can be claimed. Casualty and theft losses can be carried back three years or forward for up to 20 years.

Can a theft loss be deductible on a tax return?

A theft loss can only be deductible if the taxpayer can prove with hard evidence that the loss was caused by theft. A couple owns a house that is perched on a cliff, along with the rest of the neighborhood, overlooking the city. Unfortunately, erosion causes several houses adjacent to their property to collapse and fall over the cliff.

Are there any losses that do not qualify for a tax deduction?

However, there are several types of losses that would not qualify for deduction: Those incurred due to long-term processes, such as erosion, drought, decomposition of wood or termite damage. Any loss that arises from what the Internal Revenue Agency (IRS) considers to be a “foreseeable” event.

How do you claim losses from crypto currency theft?

Generally, whether a theft occurred for tax purposes would be based on laws in the jurisdiction where the theft occurred and, and it occurred with criminal intent. A conviction is not required to determine a theft occurred (Revenue Ruling 2009-09). A capital gain/loss is the loss on the disposition of a capital asset.