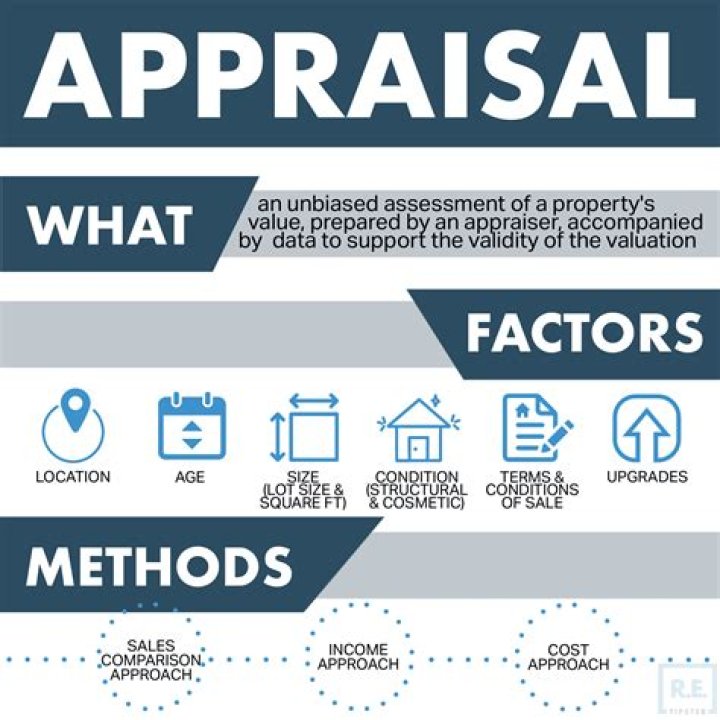

If the appraisal is deem to not be a qualified appraisal, then the taxpayer’s gift tax return may be disallowed by the Internal Revenue Service. A qualified appraisal is an appraisal document prepared by a qualified appraiser in accordance with generally accepted appraisal standards.

How do you value real estate for gift tax?

For gift and estate tax purposes, the fair market value of property transferred to another party is measured on the date of the transfer as “the price at which the property would change hands between a [hypothetical] willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both …

When appreciated property is transferred the gift tax is based on?

Transcribed image text: 1) When property is transferred, the gift tax is based on replacement cost of the transferred property fair market value on the date of transfer the transferor’s original cost of the transferred property the transferor’s depreciated cost of the transferred property D.

What proof do you need for donations?

Proof can be provided in the form of an official receipt or invoice from the receiving charitable organization, but can also be provided via credit card statements or other financial records detailing the donation.

Is the tax value a fair market value?

The assessed value of a property is typically a fractional amount of the property’s fair market value that qualifies for taxation.

When are appraisals required for a charitable donation?

When Are Appraisals Required for Donations? Any donor who claims a charitable deduction of $5,000 or more must obtain a qualified appraisal of the item’s value.

When do you need an appraisal for a gift?

Paperwork must accompany the tax return,including IRS Form 8283 and any required appraisal reports. The appraisal may have been made at any time subsequent to the date of donation and preceding the tax filing, but must be effective as of the date of donation or no more than 60 days preceding the date of the deed of gift.

Can a nonprofit have more than one appraiser?

However, you cannot have a favorite appraiser who spends most of his or her time dealing with your donors. An appraiser who spends a majority of his or her time conducting appraisals for a single nonprofit cannot be a qualified appraiser under IRS rules.

When do IRS appraisals have to be completed?

Appraisals completed prior to the actual donation of the gift are limited to the date of the report, and only considered valid by the IRS up to no more than 60 days prior to the date of donation.