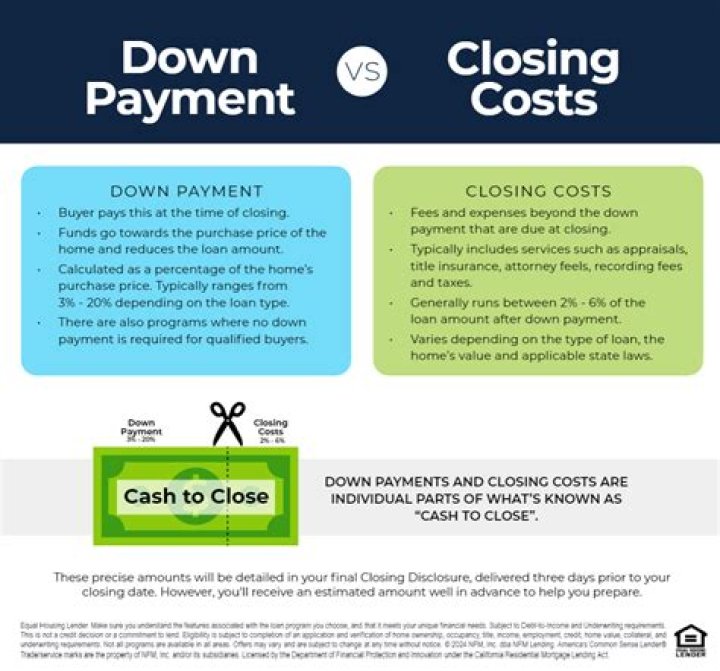

How Much is a Down Payment on a Home? Mortgage companies expect buyers to put their own money down toward the loan at closing. The down payment is separate from closing costs, but this payment is also due on closing day.

Can you roll down payment and closing costs into mortgage?

Many mortgage lenders offer what they call “no-closing cost” loans – mortgages you can roll your closing costs into rather than paying them upfront. As an investor, these loans can be tempting. After all, they reduce the amount of money you’ll need upfront to buy a property.

What does the down payment on a house go towards?

When you’re buying a home, the down payment is simply the money that you pay toward the purchase upfront. If you are, like most people, paying less than 100 percent of the home’s price out of your own pocket, you’ll have to borrow the balance of the purchase price from a lender in the form of a mortgage.

Can you use a personal loan for closing costs?

If you use a personal loan to pay for your down payment, make sure that you have enough money for closing costs. Technically a personal loan can cover both your down payment and closing costs, but this defeats the purpose of these payments and your debt-to-income ratio will likely increase.

What’s the difference between a down payment and closing cost?

Your down payment and closing costs are completely different. Being aware of how much money you’ll need to cover both is critical for qualifying for specific loan programs and closing the deal on your home purchase.

Where does the money go to pay closing costs?

Paying closing costs with a cashier’s check A cashier’s check is drawn on the issuing bank’s escrow account, so the funds are guaranteed by the bank. The funds are moved from your account (or handed over in cash) and placed in the bank’s escrow account.

What happens to earnest money if seller pays closing costs?

Click to see full answer. In respect to this, what happens to earnest money if seller pays closing costs? If that happens, the earnest money will be applied to closing costs instead of down payment. If there’s money left over after the closing costs are paid, you will get the surplus back.

Can a mortgage company refuse to pay for closing costs?

Some title companies and mortgage providers have even banned cash payments during closing. Your lender needs to know you have the money ready for closing costs in your account before they approve your loan. Credit cards allow you to borrow money from a creditor, so they’re risky for lenders.