Straight line depreciation is the easiest depreciation method to calculate. As a result, the calculation is more likely to be accurate.

How is straight line depreciation recorded?

In your accounting records, straight-line depreciation can be recorded as a debit to the depreciation expense account and a credit to the accumulated depreciation account. Accumulated depreciation is a contra asset account, so it is paired with and reduces the fixed asset account.

What is the difference between straight line depreciation and declining balance depreciation?

The straight-line method depreciates an asset by an equal amount each accounting period. The declining balance method allocates a greater amount of depreciation in the earlier years of an asset’s life than in the later years.

What is the difference between straight line and reducing balance depreciation?

The main difference between the reducing balance and straight-line methods of depreciation is that while the reducing balance method charges depreciation as a percentage of an asset’s book value, the straight-line method expenses the same amount each year.

What is reducing balance depreciation?

Reducing balance depreciation is a method of calculating depreciation whereby an asset is expensed at a set percentage. In other words, more depreciation is charged at the beginning of an asset’s lifetime and less is charged towards the end.

What is the least used depreciation method?

Straight line depreciation

Straight line depreciation is often chosen by default because it is the simplest depreciation method to apply.

Is Macrs or straight line depreciation better?

If you want to use MACRS’ Alternative Depreciation System, you have to choose straight line depreciation. ADS offers longer depreciation schedules, so if it benefits your bottom line to draw out the deduction over more years, it may be a better choice.

What is ignored in the computation of depreciation of fixed asset?

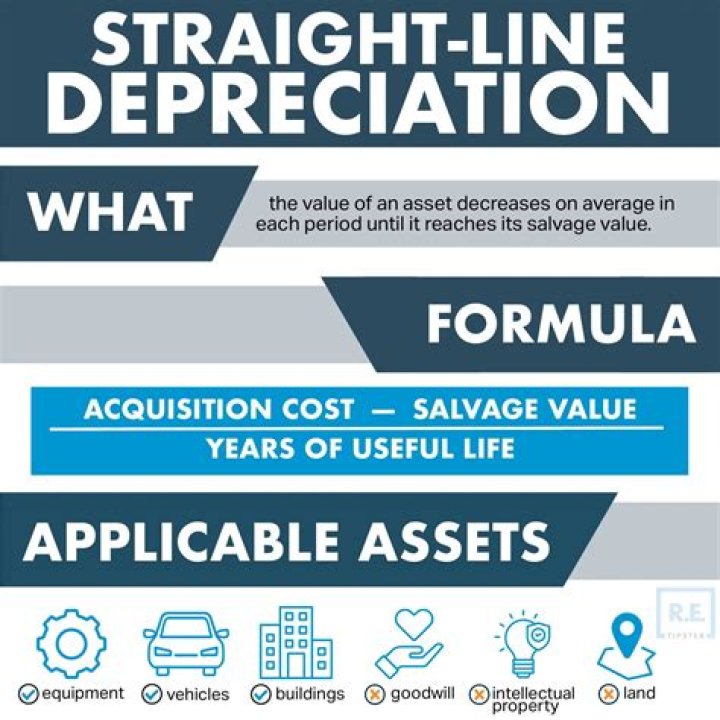

Depreciation is calculated based on the asset cost, less any estimated salvage value. If salvage value is expected to be quite small, then it is generally ignored for the purpose of calculating depreciation.

Does GAAP require depreciation?

Depreciation accounts for decreases in the value of a company’s assets over time. Accountants must adhere to generally accepted accounting principles (GAAP) for depreciation.

Why is straight line depreciation the most popular?

Straight line basis is a method of calculating depreciation and amortization, the process of expensing an asset over a longer period of time than when it was purchased. Straight line basis is popular because it is easy to calculate and understand, although it also has several drawbacks.

How is the straight line method of depreciation used?

Straight-line depreciation is a method of depreciating an asset whereby the allocation of the asset’s cost is spread evenly over its useful life. If it can later be resold, the asset’s salvage value is first subtracted from its cost to determine the depreciable cost – the cost to use for depreciation purposes.

How to calculate straight line depreciation on a MacBook?

(Five years is the period over which the IRS says you have to depreciate computers.) To determine straight-line depreciation for the MacBook, you have to calculate the following: According to straight-line depreciation, your MacBook will depreciate $300 every year.

How is the cost of depreciation lower each year?

But unlike Straight-line depreciation, the depreciable cost of the asset is lowered each year by subtracting the previous year’s depreciation. Two less-commonly used methods of depreciation are Units-of-Production and Sum-of-the-years’ digits.

When do you depreciate an asset in year 1?

For example, if an asset is put into service July 1st with a 3-year useful life, half of a year’s depreciation is allocated in year 1, a full year’s depreciation in years 2 and 3, and a half-year depreciation in the fourth year. There are three other widely-accepted depreciation methods or formulas.