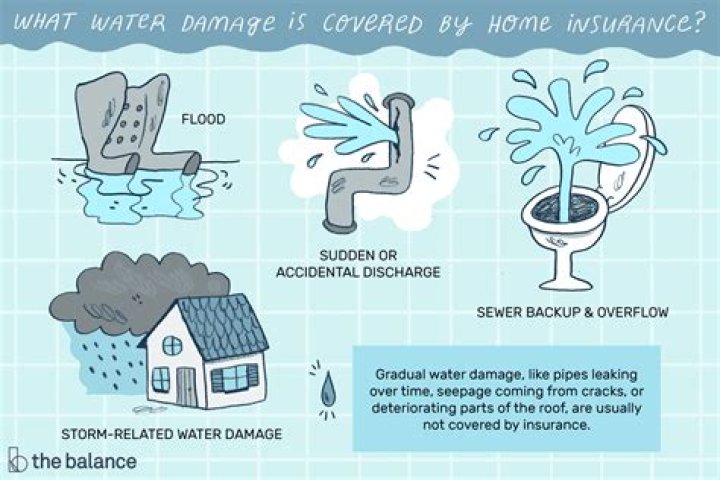

The standard California homeowners policy provides coverage for”the sudden and accidental discharge of water or steam”. Gradual water damage, like a water pipe leaking over a long period of time, is usually not covered by insurance.

How do insurance claims work for water damage?

Homeowners insurance will only cover water leaks and water damage if the cause is sudden or accidental. For example, if a pipe bursts out of nowhere, the damage will likely be covered by your insurance policy. Gradual water damage, which occurs slowly and over time, is not covered by homeowners insurance.

What is accidental water damage?

Sudden or Accidental Damage A standard homeowners insurance policy generally covers water damage that occurs due to “sudden or accidental discharge” of water, not resulting from damage from age or weathering. This could include a water heater rupture, a burst pipe, or a washing machine hose failure.

Does insurance cover accidental flooding?

Your homeowners insurance policy should cover any sudden and unexpected water damage due to a plumbing malfunction or broken pipe. However, most home insurance policies exclude damage to your home that occurred gradually, such as a slow, constant leak, as well as damage due to regional flooding.

What is the difference between water backup and water damage?

If water gets blocked from below the toilet bowl flange, backs up, and fills your bathroom floor, this is water backup. A home insurance policy includes water overflow under the water damage clause but does not cover water backup.

Does homeowners insurance cover water damage from plumbing?

Homeowners insurance may help cover damage caused by leaking plumbing if the leak is sudden and accidental, such as if a washing machine supply hose suddenly breaks or a pipe bursts. However, homeowners insurance does not cover damage resulting from poor maintenance.

Under most standard home insurance policies, if water damage occurs suddenly or accidentally from a source inside your home, such as a busted pipe, it will likely be covered by your homeowners insurance. If the water comes from outside your home, it will not be covered by your standard policy.

What happens if I make a water damage claim?

If the insurance company agrees to cover the claim, you will come to an agreement on the cost of the claim. This may be either a contractor you decide or one the insurance company designates depending on your insurance policy. Get started with the restoration of your property.

How long does it take to get a check for water damage?

You should receive a check from your insurers within five business days (if you don’t get the check on time, call the company to request it and file a complaint if necessary). You need to comply with the terms and conditions in your insurance policy in order to get your water damage claim accepted.

When to notify your insurance company about water damage?

Whether your home has been flooded by torrential rains or a leaking pipe has caused immense structural damage, the first thing to do after the imminent danger has passed is to notify your insurance company. The sooner you contact them, the quicker and more efficient the entire process will be.

Why did my insurance company not collect on my water leak?

The insurance company claimed the insured did not give “prompt notice” of their water leak. The insured did wind up collecting, but that was after a year and a half battle with the insurance company.