Nonelective contributions are funds employers choose to direct toward their eligible workers’ employer-sponsored retirement plans regardless if employees make their own contributions. These contributions come directly from the employer and are not deducted from employees’ salaries.

What are discretionary nonelective contributions?

Non-elective contributions are payments made towards an eligible employee’s retirement plan, regardless of whether the employee makes contributions to the plan or not. Non-elective contributions are not deducted from the employee’s salary and are instead funded directly from the employer’s account.

What is an NEC contribution?

An employer NEC, or nonelective contribution, includes any funds an employer gives to its employees for retirement. For example, one employer may contribute 2% of every eligible employee’s salary toward their employer-sponsored retirement plan.

What are discretionary contributions?

One option is a discretionary contribution. As described by the IRS, “If the plan document permits, the employer can make contributions other than matching contributions for participants. Employers can choose to make discretionary contributions but they are not required every year.

What is a discretionary 401k match?

Discretionary Matching Contributions allow the employer to decide which percentage of employee deferrals to match and provides the employer with the ability to adjust matching amounts as business needs change.

What are qualified matching contributions?

Qualified Matching Contributions (QMACs) are like QNECs, except rather than being non-elective, they are matching contributions, made as a percentage of the employee’s elective deferral. They are typically used to help you pass the ACP test — much the same way that QNECs are used to help you pass the ADP test.

What is a qualified match?

Qualified Matching Contribution means any Matching Contribution made to the Plan as provided in Article VI that is 100 percent vested when made and may be taken into account to satisfy the limitations on 401(k) Contributions made by Highly Compensated Employees under Article VII.

What is a deferral contribution?

Key Takeaways. An elective-deferral contribution is a portion of an employee’s salary that’s withheld and transferred into a retirement plan such as a 401(k). Elective-deferrals can be made on a pre-tax or after-tax basis if an employer allows.

What are elective contributions?

Elective Deferrals are amounts contributed to a plan by the employer at the employee’s election and which, except to the extent they are designated Roth contributions, are excludable from the employee’s gross income. Elective deferrals include deferrals under a 401(k), 403(b), SARSEP and SIMPLE IRA plan.

Why do companies make discretionary contributions?

What is the definition of a nonelective contribution?

What is a ‘Nonelective Contribution’. Nonelective contributions are funds employers choose to direct toward their eligible workers’ employer-sponsored retirement plans regardless if employees make their own contributions. These contributions come directly from the employer and are not deducted from employees’ salaries.

Are there limits to how much an employer can contribute to a nonelective organization?

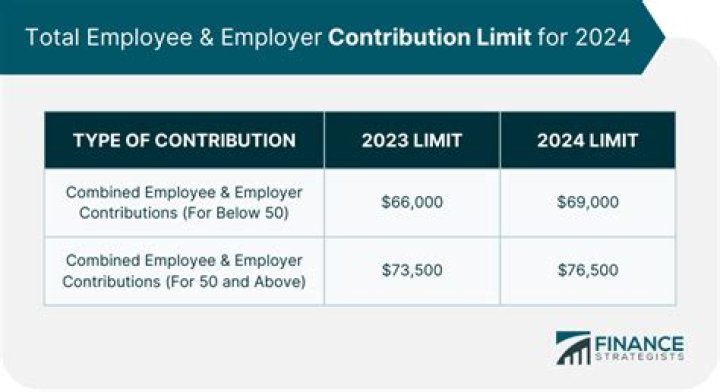

Employers are free to change the contribution rates as they see fit for their organizations. However, nonelective contributions can not exceed the annual contribution limits set by the Internal Revenue Service (IRS).

How does an employer contribute to a non elective plan?

The amount that an employer contributes towards a non-elective contribution varies from one employer to another. An employer is free to set or change the non-elective contribution rates as they see fit. However, the amount that an employer contributes towards the plan should not exceed the limits set by the US Internal Revenue Service (IRS).

What are the benefits of a fully vested nonelective contribution?

The decision to offer fully-vested nonelective contributions can also provide retirement plans with Safe Harbor protection, which exempts plans from government-mandated nondiscrimination testing. The IRS administers these tests to make sure plans are designed to benefit all employees instead of favoring highly-compensated ones.