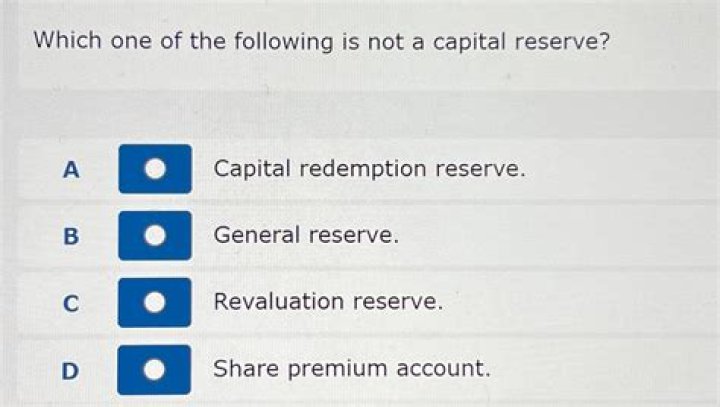

The correct answer is B.

What are the different types of reserve fund?

There are different types of reserves used in financial accounting like capital reserves, revenue reserves, statutory reserves, realized reserves, unrealized reserves.

What is reserve fund in corporate accounting?

A reserve fund is a savings account or other highly liquid asset set aside by an individual or business to meet any future costs or financial obligations, especially those arising unexpectedly. If the fund is set up to meet the costs of scheduled upgrades, less liquid assets may be used.

How big should a reserve fund be?

In general, funds need at least $2,000 per unit per year to avoid under funding. An average for a new building might be just $500 per unit per year while older buildings can be as much as $4,000.

Is not capital reserve?

Dividend Equalization Reserve – It is revenue reserve that serves as a buffer between a certain dividend level and profits available. Sums are transferred to this reserve account in good years, and withdrawn from in poor years to maintain the dividend amount.

Why is reserve fund a liability?

Reserves are considered on the liability side of a balance sheet because they are sums of money that have been set aside to be paid out at a future date. As these reserves don’t actually belong to the company, they are not considered assets but liabilities.

How do you record reserve funds?

Generally, you debit retained earnings and credit the reserve fund (also an equity account). All this does is set the funds aside for a specific purpose. For presentation purposes, the reserve fund account can be a separate account or a sub-account in the equity section of your balance sheet.

Why capital reserve is a liability?

A capital reserve is an anachronism because the term “reserve” is not defined under generally accepted accounting principles (GAAP). Sums allocated to a capital reserve are permanently invested and cannot be used to pay dividends to shareholders.