The employer match also is an attractive benefit for recruitment. If an employee has offers from more than one company and all else is equal, the 401(k) contribution matching could become a factor in choosing one firm over another. Also, employers receive tax benefits for contributing to 401(k) accounts.

What if your job doesn’t offer 401K?

The most obvious replacement for a 401(k) is an individual retirement account (IRA). Since an IRA isn’t attached to an employer and can be opened by just about anyone, it’s probably a good idea for every worker—with or without access to an employer plan—to contribute to an IRA (or, if possible, a Roth IRA).

As mentioned earlier, 401k plans are tax-deductible for employers. Because 401k plans have several tax benefits, they are usually less expensive to offer than defined-benefit plans. The good news is that usually, every dollar a company contributes to a staff member’s 401k is a write-off.

What can I contribute to my 401k?

Most financial planning studies suggest that the ideal contribution percentage to save for retirement is between 15% and 20% of gross income. These contributions could be made into a 401(k) plan, 401(k) match received from an employer, IRA, Roth IRA, and/or taxable accounts.

Should I contribute to my 401k if my employer does not match?

As you can see from the facts above, you should absolutely invest in a 401(k) without a company match. But just make sure that you first save money in an emergency fund, and then fully fund an IRA, before making contributions to the 401(k).

How much can an employer contribute to a 401k?

For 2019, that limit stands at $56,000. This means that together, you and your employer can contribute up to $56,000 for your 401(k). If you contribute the max of $19,000, your employer can contribute up to $37,000 for 2019. For 2020, you and your employer can contribute up to $57,000.

What are three advantages of 401K accounts?

Here are 5 benefits of most traditional 401(k) plans:

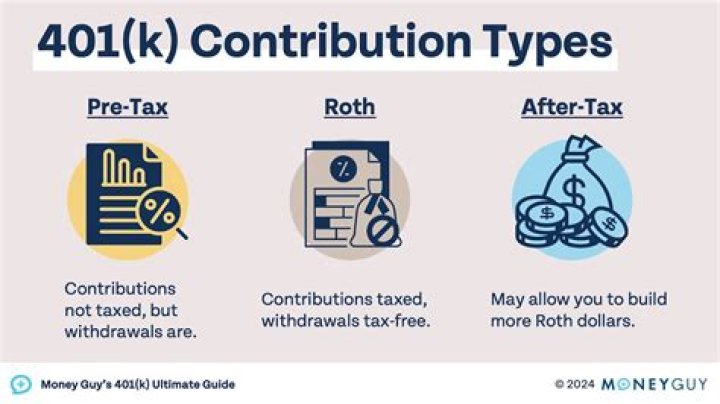

- Tax advantages. Contributions to a traditional 401(k) are taken directly out of your paycheck before federal income taxes are withheld.

- You are in control.

- Time is on your side.

- You can take it with you.

- Easy payroll deductions.

How much money can an employer contribute to a 401K?

The employer’s 401(k) max contribution limit is much more liberal. Altogether, the maximum that can be contributed to your 401(k) plan between both you and your employer is $58,000 in 2021, up from $57,000 in 2020.

How does an employer contribute to a 401k plan?

Employer Contributions. Many employers will make contributions to your 401(k) plan for you. There are three main types of employer contributions: matching, non-elective, and profit sharing. Employer contributions are always pre-tax, which means when they are withdrawn in retirement, they will be taxable at that time.

Is there an annual limit on employer contributions to 401k?

The employer contribution can be profit-sharing, matching, or safe harbor funding. For 2020, the annual additions limit for employee and employer combined contributions to defined contribution plans (like a 401 (k), 403 (b), or SEP IRA) is $57,000 for those under the age of 50.

Is it worth contributing to an employer matching 401k?

Even if your employer’s 401 (k) has high fees, it is worth contributing up to the matching limit for the immediate return. Once you’ve hit the matching limit you can consider whether other savings strategies, such as opening an IRA may be better for you.

How old do you have to be to contribute to a 401k?

To encourage workers nearing retirement to speed up their saving, the IRS allows 401(k) participants ages 50 and over to make additional contributions beyond the standard contribution limit.